When COVID-19 bludgeoned the world into submission, it tanked the economy and caused oil prices to go as low as $20. However, the technology industry had a huge financial boost as the Fintech industry recorded 100 times their revenue, most of which raked in during the high points of the pandemic.

The stay-at-home order across the world had a positive spill-back effect on digital adoption and use of technology for financial services, especially in Sub-Saharan African countries.

In Nigeria, the ICT industry contributed 14.07% and 17.83% to the country’s GDP in the first and second quarters of 2020. Some Nigeria Fintech platforms also recorded huge growth. The Africa-focused payments company, Flutterwave, noted that it recorded more than 100% in revenue within the past year because of the pandemic which contributed to its compound annual growth rate (CAGR). On the other hand, the oil sector contributed an average of 9.2% to GDP in the first and second quarters.

Nigeria’s ICT sector has grown from less than 1 percent of GDP in 2001 to almost 10 percent in 2018, and over 15 percent in 2020, surpassing South Africa to emerge as a premier investment destination with 55 active tech hubs.

A survey conducted by ONE campaign in 2019 revealed software provision, website and application development, e-commerce and retail platform, integration of tech solutions for the private and public sector are the major areas in Nigeria’s tech space while the Fintech ecosystem in the country encompasses asset management, advisory services, big data, biometrics, peer-to-peer lending, crowd computing, digital payments, and blockchain among others.

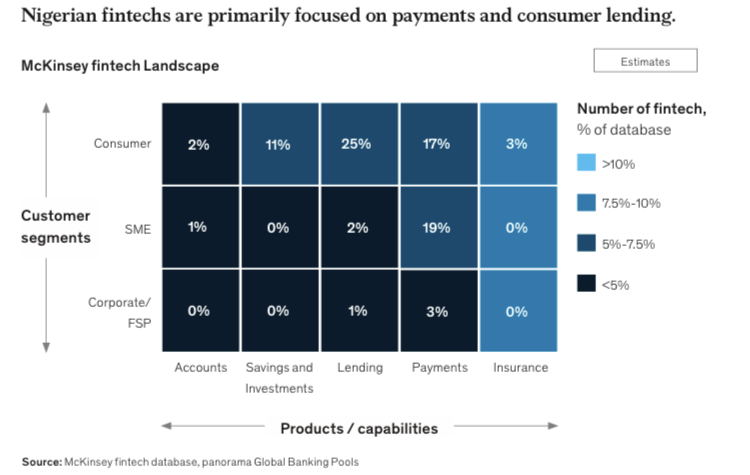

Financing, lending, payments, and remittances currently account for 69% of Nigeria’s Fintech landscape, leaving 31% to relatively untapped categories such as crowd computing, big data, business solutions, insurance, and wealth management.

Nigeria went from attracting 24% of $185 million funding raised by African tech startups in 2015 to becoming the most sought-after tech investment destination, accounting for 47.6% of the $701.5 million raised in 2020. Top gainers were Flutterwave, 54 gene, Helium health, Kuda bank, TradeDepot, Field intelligence, Medsaf, Autochek, and Rensource as they raised about $100 million within the period.

In the same year, Nigeria recorded the biggest startup acquisition as an international Fintech company, Stripe, acquired Nigerian-grown payment services, Paystack, in a deal worth over $200 million.

This news was received with massive accolades for Nigeria’s growing Fintech ecosystem. Few months after Paystack’s acquisition, another Nigerian-grown payments company, Flutterwave, announced that it raised $170m in its series C funding, pitching its valuation at over one billion dollars to achieve a Fintech Unicorn status.

The tech industry, mainly anchored by the Fintech ecosystem is steadily becoming the country’s new resource and has set a template for the future of work in Africa’s most populous nation.

Nigeria has one of the most vibrant tech hubs in Africa creating value and solving age-long problems through technological innovation and inventions, championed by Angel investors, Mobile Applications Developers, Systems Analysts, Software Developers/Programmers, Web Developers, Development Operations (DevOps) Engineers, Cybersecurity Analysts, Data Analysts, User Interface Researchers, Social Media Managers and other job descriptions within the ecosystem.

For Nigeria’s millennials and Gen-Z, data and tech is their crude oil, the choice to identify with the growing ecosystem has been made simpler by the fluctuations in global oil prices, the corruption inherent in export and import of petroleum products, and irregularities in PMS prices in the country and the multiplier economy in e-commerce, payment, and services industry.

Recall that crypto restrictions opened up the Nigerian market to innovative scrambles on how to trade, the ban on motorcycle ride-hailing services by the Lagos state government also opened up new markets for services and the food industry. The linkages in Nigeria’s economy are multifaceted and over-reliance on oyel money cannot create sustainable development for the country.

The state and the federal government should stop the carrot and stick approach extended to the tech space and Fintech ecosystem but make policies to further integrate it into the economy as obvious evidence shows it is ripe enough to topple or diversify from the age-long overburdened oil economy.

Olakunle explores the interlink of public policy, development, education, and being Nigerian. He tweets @Olakunile.

First appeared in Ominira Initiative.

Photo by Femovier via Iwaria.